Paying off your home loan in full is a major financial milestone; it means financial freedom and full ownership of your property. Whether you’re closing your account with a private bank like BDO or BPI, or with a government agency such as the Pag‑IBIG Fund, the process follows a similar set of steps. In this blog, I’ll walk you through the step-by-step process for full payment of a bank’s home loan, using my own experience with BDO as an example.

Context: In my case, the full payment was actually part of a refinancing. I’ll focus here on the full payment process itself, and I have a separate blog dedicated to the refinancing journey.

Step 1: Contact Your Lender

Reach out to your bank or lending institution to express your intent to fully settle your loan. For banks: you can visit a branch or contact their loan servicing department. For Pag‑IBIG: coordinate with their loan management office.

I sent an e-mail to loans-aftersales@bdo.com.ph, asking what is the process of full payment for my home loan.

Step 2: Request a Payoff Statement

Lenders use different names for their payoff statement but it serves the same purpose. This document shows the exact amount you need to settle, including principal, interest, and fees. When requesting, you must provide the borrower’s name, contact information, loan account number, Promissory Note (ON) number, and the preferred pay-off date. The payoff statement is valid only for a specific date and cannot fall on a non‑banking day.

Terms Used by Major Philippine Lenders

- BDO: Statement of Account for Full Payment

- BPI: Statement of Account to Fully Pay

- Metrobank: Payoff Statement / Loan Payoff Computation (generic term used by loan servicing)

- Chinabank: Statement of Account

- RCBC: Payoff Statement / Loan Payoff Computation (generic term used by loan servicing)

- EastWest Bank: Loan Payoff Computation / Statement of Account for Loan Settlement

- Pag‑IBIG Fund: Statement of Account (SOA) / Loan Balance Computation

Processing Time

Banks usually take a few days to process your request. The summary below outlines the typical processing times across major banks:

- BDO: ~3 banking days

- BPI: ~1–2 banking days

- Metrobank: ~2–3 banking days (general industry practice; timeline not formally published)

- Chinabank: 1–3 banking days

- RCBC: ~2–3 banking days (general industry practice; timeline not formally published)

- EastWest Bank: ~2–3 banking days (general industry practice; timeline not formally published)

- Pag‑IBIG Fund: several days; tied to settlement date

I requested for SOA for full payment from BDO via email (loans-aftersales@bdo.com.ph). You can also request for SOA for full payment by filling out the BDO Home Loan Full Payment Computation Form. I received my SOA for full payment 3 banking days after sending BDO an e-mail request.

Step 3: Confirm the Amount and Date

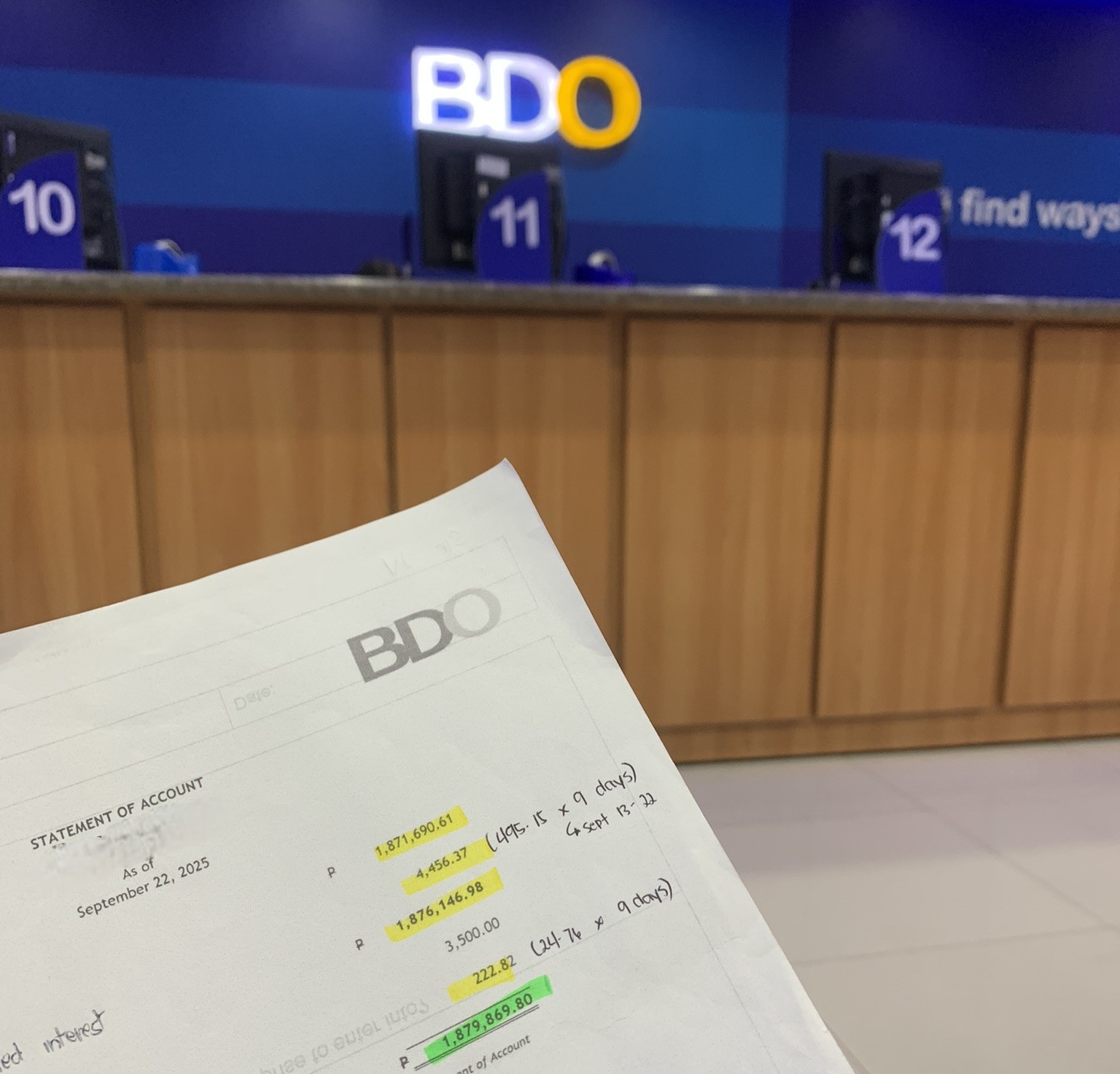

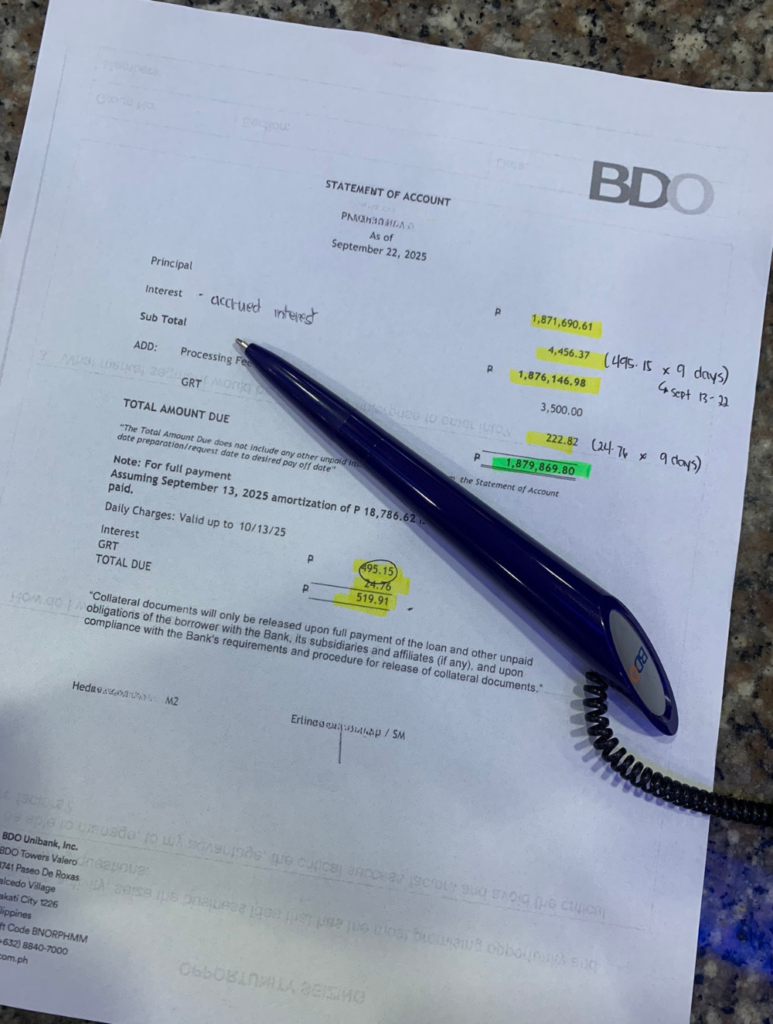

Once the computation is ready, you’ll get the exact amount to settle, which includes remaining principal balance, accrued interest, pre-termination fees (if applicable), processing fees, and other charges (like Gross Receipts Tax or GRT). Double‑check the exact amount and the payment date. Ensure you have the funds ready before the validity date.

Gross Receipts Tax (GRT) is a tax on the bank’s earnings, passed on to borrowers, which directly affects the loan payoff amount. When preparing for full payment, expect GRT to be part of the computation alongside interest and fees.

My outstanding balance was ₱1,871,690.61, plus accrued interest, GRT, and processing fees, bringing the total to ₱1,879,869.80.

Step 4: Settlement of Balance

Settle the confirmed amount through your lender’s accepted payment channels, which may include cash (over‑the‑counter), manager’s checks, post‑dated checks (PDCs), online banking transfers, or auto‑debit arrangements, depending on the bank. Pag‑IBIG Fund offers the widest range of channels, including e‑wallets and payment centers. Make sure the payment is made on or before the specified date to avoid discrepancies. Paying later than the specified date may result in additional interest charges.

I settled the payment over‑the‑counter at the nearest BDO branch. Since I was unable to pay on the stated pay‑off date, the account accrued daily interest of ₱495.15 for four days. This increased the previous total amount due of ₱1,879,869.80 by ₱1,980.60, bringing the final settlement amount to ₱1,881,846.40. In line with BDO’s instructions, I then e‑mailed them a scanned copy of the official receipt to facilitate the processing of my payment.

Step 5: Release of Loan Documents

After your payment is processed (usually within a few banking days), the lender will confirm that your loan is fully settled. The original property title will be returned with the mortgage lien cancelled, along with other supporting documents such as the notarized Release of Mortgage, the cancelled Promissory Note, and a Loan Closure Certificate or equivalent clearance.

It took eight banking days for BDO to acknowledge my e‑mail regarding the payment made. Seven banking days later, I received another e‑mail informing me that I could now claim my collateral documents. The message included instructions on how to set an appointment through the BDO website, as the bank strictly enforces a No Appointment, No Release policy. Take note: if you fail to claim your documents within a reasonable time, the bank may impose safekeeping fees.

Step 6: Title Clearance

The final step is to clear your property title at the Registry of Deeds (RD). This process removes the mortgage annotation and officially renders your property free of encumbrances. For a detailed guide, read my blog: How to Cancel Real Estate Mortgage (REM)?

Why Pay Off Early?

Many homeowners wonder if it’s worth paying off their mortgage before the end of the loan term. While it depends on your financial situation, here are some common reasons why it is ideal to settle early:

- Save on Interest: The longer your loan runs, the more interest you pay. By closing it early, you reduce the total interest cost significantly.

- Avoid Repricing Risks: Banks often reprice housing loan interest rates every few years. Paying off early protects you from sudden increases in monthly amortization.

- Full Ownership of Property: Once the mortgage annotation is cancelled at the Registry of Deeds, your property is officially free from encumbrances.

- Peace of Mind: Being debt-free means less financial stress and more flexibility in managing your income.

- Better Financial Planning: With no monthly amortization, you can redirect funds toward investments, retirement savings, or other priorities.

- Refinancing Opportunities: Some borrowers pay off their loan early because they’re refinancing with another bank for better terms. (In my case, my full payment was part of a refinancing move. Read my blog on how I refinanced my home loan and saved ₱1.8 million in interest payments.)

Important Notes & Practical Tips

- PN Number: Prepare your Promissory Note number early; it’s crucial for requesting your Statement of Account.

- Pay‑off Date: Set a clear target date and inform the bank so they compute accurately.

- Timing: Interest accrues daily, so paying late, even by a few days, can increase your balance.

- Fees & Penalties: Some lenders may charge processing or pre‑termination fees for early settlement.

- Insurance: Mortgage Redemption Insurance (MRI) coverage typically ends with the loan. Fire insurance may need to be handled separately, as you are now the full owner.

- Follow‑ups: Don’t wait for the bank to contact you—send polite reminders if acknowledgment is delayed.

- Document Release: Schedule your claim promptly. Banks may charge safekeeping fees if collateral documents aren’t collected on time.

- Documentation: Keep all receipts and clearance documents safe. You’ll need them for title transfer or dealings with the Registry of Deeds.

Closing a home loan may feel tedious, but with preparation and persistence, it’s manageable. More than just settling a balance, it’s about securing full ownership and ensuring your property is legally free and clear. Congratulations in advance on taking steps toward financial freedom, whether you’re paying in full now or simply learning how. God bless on your homeownership journey.